AleksandarNakic/E+ via Getty Images

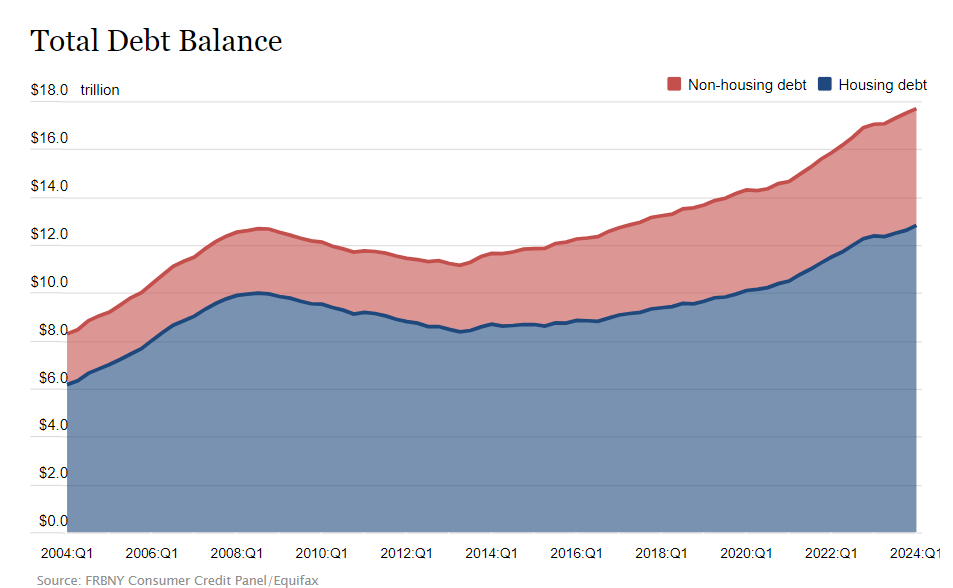

The overall debt accumulated by U.S. households increased during the first quarter, climbing by $184B, or 1.1%, to $17.69T, as the rates of credit card and auto loan transitions into serious delinquency persisted in their upward trend, according to the Federal Reserve Bank of New York’s Household Debt and Credit Report published Thursday.

Total debt levels are some $3.5T above where they were at the end of 2019, before the pandemic hit.

During the quarter, mortgage balances increased by $190B to $12.44T, and auto loan balances advanced by $9B to $1.62T. Credit card balances decreased by $14B at the end of March to $1.12T, but they remain about 13% above the year-ago level.

“Credit card balances have never risen from the fourth quarter of one year to the first quarter of the next year since the New York Fed initiated this data set in 2003 (balances were flat from Q4 2022 to Q1 2023),” noted Ted Rossman, senior industry analyst at Bankrate. “Americans typically engage in a post-holiday financial detox in Q1.”

The New York Fed report showed that overall delinquency rates ticked up to 3.2% from 3.1% in the previous quarter. Even so, the latest mark trails the 4.7% seen at end-2019.

But “An increasing number of borrowers missed credit card payments, revealing worsening financial distress among some households,” said Joelle Scally, regional economic principal within the Household and Public Policy Research Division at the New York Fed.

Some 8.9% of credit card accounts and 7.9% of auto loan accounts moved into troubled status on an annualized basis. Delinquency transition rates for mortgages rose by 0.3 percentage point, though they remain “low by historical standards,” the report said.