L T Foods Ltd. – Farm to Fork

Incorporated in 1990, LT Foods Ltd. is a global consumer food company specializing in basmati and other specialty rice, organic foods, ingredients, and ready-to-eat/ready-to-cook segments. It is the leading rice brand in India and the No. 1 specialty food brand in the US, with flagship brands like ‘Daawat’ and ‘Royal’. The company holds a market share of over 29% in India and nearly 50% in the US basmati market, distributing its products across 80+ countries.

Products and Services

- Rice Portfolio: Includes brown, white, steamed, parboiled, organic, and quick cooking brown flavored rice under brands like Daawat, Royal, Heritage, Gold Seal Indus Valley, 817 Elephant, Devaaya, and Rozana.

- Organic Foods: Comprises rice, soya, pulses, oil seeds, cereal grains, spices, and nuts.

- Rice-Based Convenience Products: Sauté sauces, cuppa rice, ready-to-heat products, fortified rice, and rice-based premium snacks.

Subsidiaries: As of FY23, LT Foods has:

- 15 subsidiaries

- 3 associate companies

- 3 joint ventures

Growth Strategies

- Established Brand: Strong portfolio with brands like Daawat and Royal; domestic market share at 30.1% with a volume growth of 11% in FY24.

- Global Market Dominance: Expanding product portfolio and efficiency; significant growth in the US and Middle East markets.

- Strategic Deals and Expansion: Entered new markets and strategic deals, including with SALIC and in countries like Tanzania and Zambia.

- New Facility: Upcoming facility in the UK to enhance production capabilities.

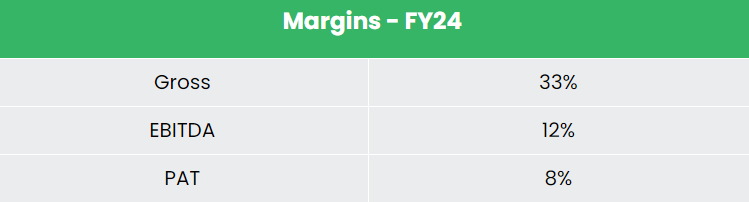

Financial Highlights

Q4FY24

- Revenue Growth: 14% YoY increase to Rs. 2,092 crore in Q4FY24 from Rs. 1,835 crore in Q4FY23.

- EBITDA Improvement: Grew by 25% to Rs. 262 crore in Q4FY24 from Rs. 210 crore in Q4FY23.

- EBITDA Margin Expansion: Increased by 110 bps to 12.5% due to lower input costs, higher realisation, and normalised freight costs.

- Net Profit Increase: 14% rise to Rs. 150 crore in Q4FY24 from Rs. 132 crore in Q4FY23.

FY24

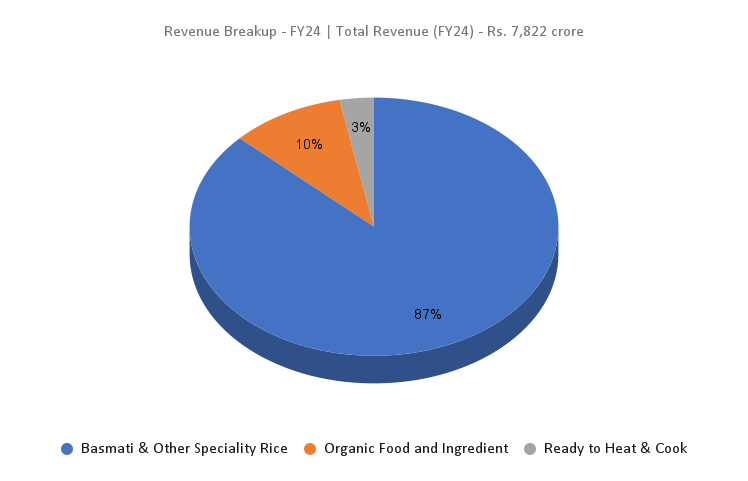

- Revenue Growth: ₹7,822 crore, an increase of 12% YoY

- Basmati and Specialty Rice Segment: Grew by 17%

- Ready-to-Eat and Ready-to-Cook Segment: Grew by 23%

- Operating Profit: ₹988 crore, up 33% YoY

- Net Profit: ₹598 crore, an increase of 41% YoY

Financial Performance (FY21-24)

- Revenue and PAT CAGR: 18% and 29% respectively, over three years.

- Average ROE and ROCE: Approximately 18% for FY 21-24 period.

- Capital Structure: The company maintains a robust capital structure with a debt-to-equity ratio of 0.27.

Industry outlook

- The Indian food processing sector is a priority under the “Make in India” initiative.

- Accounts for 32% of the country’s total food market, ranked fifth globally.

- Significant potential for value addition, with exports of 11.1 Mn Tonnes of non-basmati rice and 5.2 Mn Tonnes of basmati rice in FY 23-24.

- Growing demand for organic products, expected to rise with a CAGR of 25.25% from 2022-27.

Growth Drivers

- FDI: 100% FDI permitted under the automatic route in food processing industries.

- Budget Allocation: ₹3,290 crore allocated for the Ministry of Food Processing Industries in the Interim Budget 2024-25, a 13% increase.

- Market Size: Projected to reach US$ 1,274 billion by 2027 from US$ 866 billion in 2022.

Competitive Advantage

KRBL is the only listed competitor of LT Foods at a comparable market cap and range of operations. LT Foods shows higher return ratios and stable revenue growth, indicating better financial stability and efficiency.

Outlook

- Brand Presence: Focus on brand building, innovation, and international expansion.

- Growth Targets: Aiming for a 5-year revenue CAGR of 10-12%, with a plan to increase the 5-year EBITDA margin by 140-150 basis points.

- Return Ratios: Targeting ROCE of 23% and ROE of 20% by FY24-25.

- Challenges: Navigating issues like anti-dumping duty in the soya market and margin pressures from freight costs.

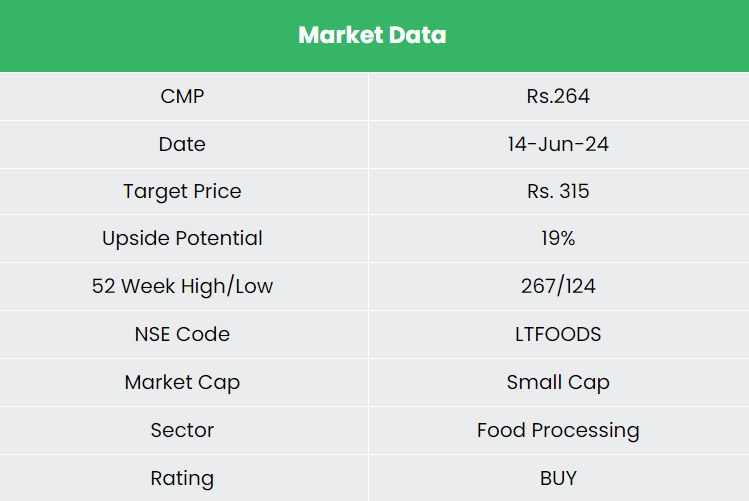

Valuation

LT Foods Ltd. has robust growth prospects given its strong focus on strengthening brands, distribution, and region & product diversification. We recommend a BUY rating in the stock with the target price (TP) of Rs. 315, 11x FY26E EPS.

Risks

- Forex Risk: Exposure due to significant operations in foreign markets.

- Socio-Economic Risk: Potential impact from socio-economic instability leading to increased input costs.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.

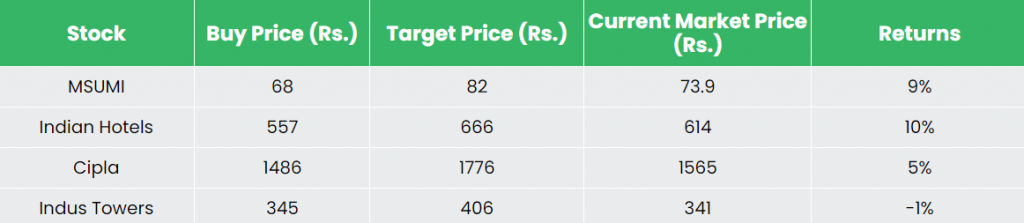

Recap of our previous recommendations (As on 14 June 2024)

Motherson Sumi Wiring India Ltd

Indian Hotels Co Ltd

Cipla Ltd

Indus Towers Ltd

Other articles you may like

Post Views:

34